What is the Difference Between Public and Private Commercial Real Estate Credit?

Many advisors considering a commercial real estate (CRE) credit allocation often ask about the difference between public and private CRE credit. Let’s address that question in this discussion.

CRE Credit: Public or Private?

- Public CRE credit, or indirect lending through publicly traded securitized mortgage loans such as mortgage REITs, can provide investors income from borrowers’ mortgage loan payments.

- Private CRE credit, also commonly referred to as debt, provides real estate exposure through direct mortgage loan lending. CRE credit investment vehicles originate loans to qualified borrowers using income-producing properties as collateral to back the loans. Mortgage loan payments from the borrower can provide income to the investor during the life of the loan.

Important Tradeoffs

Public CRE credit investments offer investors the advantage of liquidity, which may be a significant factor for many of your clients. On the other hand, as publicly traded securities, these investments can often be subject to the broader movement of the markets and other asset classes, increasing portfolio volatility.

Private CRE credit investments are considered illiquid, which can deter some investors.

Also, private CRE credit investments sit at the top of the commercial real estate capital structure, meaning they are top priority in terms of payment, and are secured by the underlying properties, which can provide investors with a higher degree of security in the event a property owner defaults.

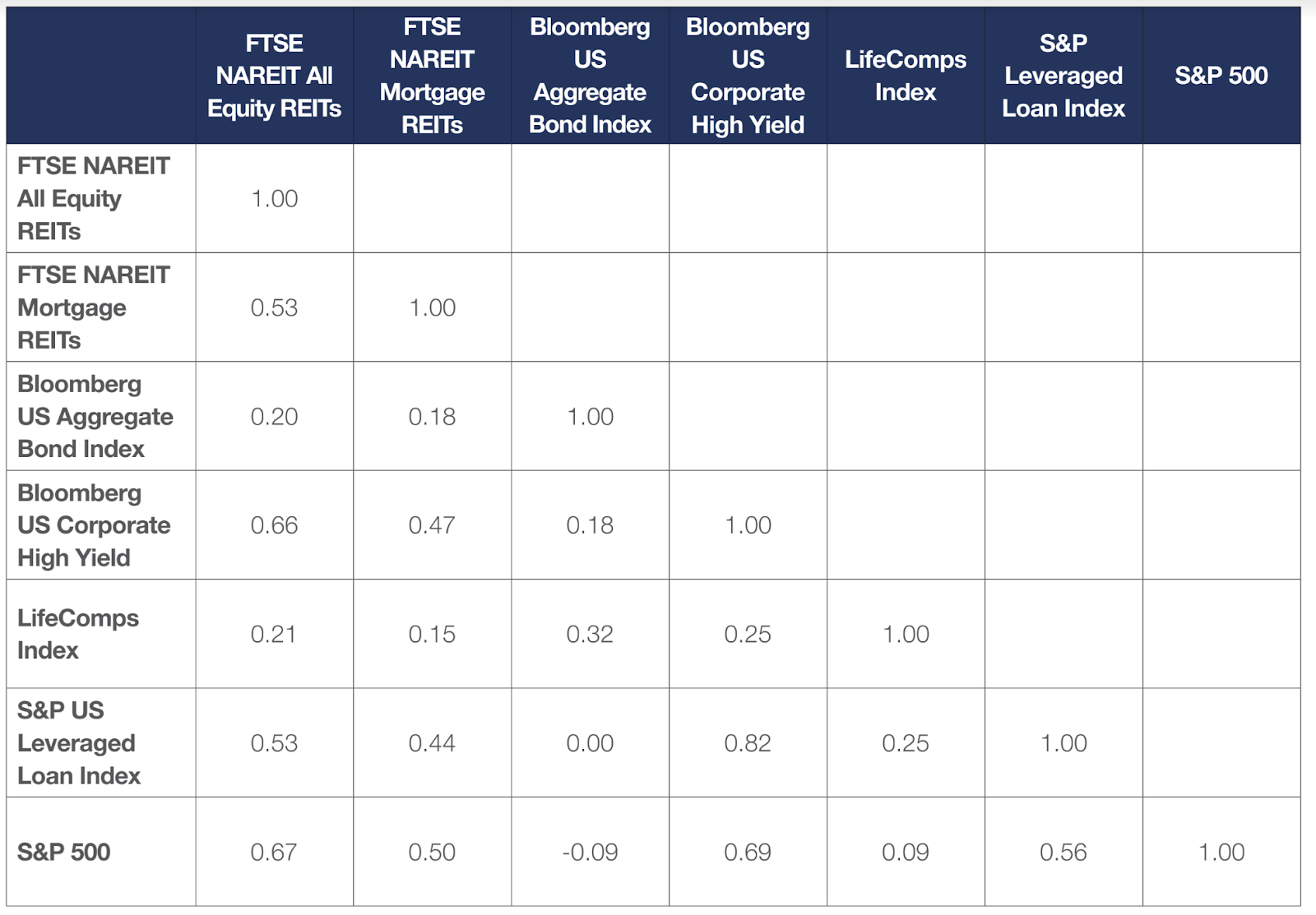

Correlation Matters

When considering an allocation to private CRE credit, it's essential to understand the correlation between investment options to help ensure you are achieving the desired portfolio diversification by adding an alternative asset class.

As you may know, the lower the correlation between two investments, the less likely they will move up and down at the same time or to the same relative degree. A correlation of 0 means that price fluctuations are not correlated at all, and a negative correlation means that investments move in the opposite direction.

This chart below shows that private CRE credit (as represented by the LifeComps Index) has exhibited the lowest correlation to public equity and bond indices of any asset class over the last twenty years.

|

20-Year Commercial Real Estate Correlation Review |

|

| Source: MorningStar Direct. The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. The FTSE Nareit Mortgage REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. Mortgage REITs. The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar denominated, fixed-rate taxable bond market. The Bloomberg USD High-Yield Corporate Bond Index is a rules-based, market-value-weighted index engineered to measure publicly issued non-investment grade USD fixed-rate, taxable and corporate bonds. The LifeComps Commercial Mortgage Loan Index measures actual private commercial mortgage market loan cash flow and performance data collected quarterly from participating life insurance companies since 1996. Commercial mortgages may be subject to default risk. The S&P US/LSTA Leveraged Loan Index is designed to reflect the performance of the largest facilities in the leveraged loan market. The S&P 500 is a float-weighted index, meaning the market capitalizations of the companies in the index are adjusted by the number of shares available for public trading. |